The new technologies needed to generate low-carbon energy and transition to a green economy are demanding ever-growing quantities of critical minerals. These minerals exist in abundance around the world, but extracting and processing them is expensive, technically demanding, and energy-intensive.

Manufacturing solar panels, wind turbines, and electric vehicles requires far more minerals than their fossil fuel-based alternatives. A typical electric vehicle needs six times more of these resources than a conventional car, and an offshore wind farm needs thirteen times more than a gas-fired power plant.

Given that no single universal definition exists, different countries designate minerals as critical based on their own economic and geopolitical circumstances. The US and EU consider close to 50 minerals critical, including:

- Lithium, graphite, cobalt, nickel, and manganese — used in electric vehicle batteries

- Silicon and tin — used in electric vehicles, transmission networks, electricity meters, and other devices

- Rare earth elements — used in wind turbine magnets and electric vehicles

- Copper — used in transmission networks, wind farms, and electric vehicles

- Gallium and germanium — used in solar panels, electric vehicles, defense radars, lasers, and more

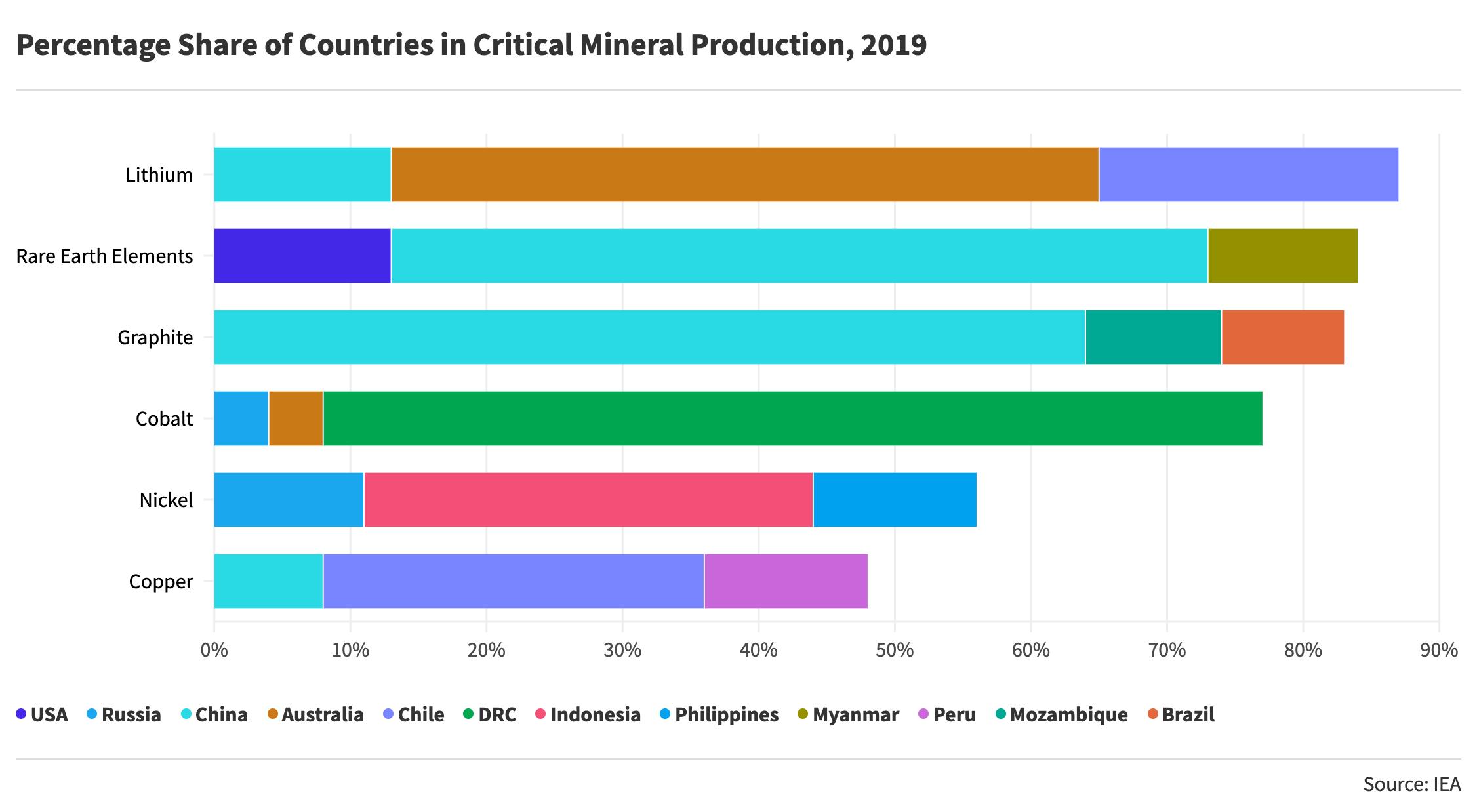

These resources are primarily found in China, the Democratic Republic of Congo, South Africa, Indonesia, Chile, Australia, and in smaller quantities in other countries.

As the importance of renewable energy grows, demand for these minerals is rising sharply — pushing up prices and reshaping the market for energy transition minerals, whose total capitalization has doubled over the past five years, reaching $320 billion in 2022.

Under various scenarios from the International Energy Agency (IEA), demand for critical minerals could double or grow 3.5 times by 2030.

Investment has kept pace: it grew 20% in 2021 and 30% in 2022. Notably, Chinese companies nearly doubled their investments in 2022 alone.

According to the International Renewable Energy Agency (IRENA), a gap between supply and demand is already visible, particularly for lithium. While supply disruptions have minimal impact on energy security for now, they are critical for the energy transition.

The IEA says that if all currently planned projects worldwide are carried out, critical mineral supply should not be at risk. But several risks remain — and one of the biggest is China’s dominance.

China’s Dominance

China’s former leader Deng Xiaoping was talking about the importance of critical minerals as far back as 1992. “The Middle East has oil; China has rare earths,” he said.

As the country’s economy grew, domestic demand for industrial goods outpaced local supply. China responded by investing beyond its borders, steadily expanding its influence in every direction and securing a monopoly position.

Cobalt, for example, is mined in the Democratic Republic of Congo but largely controlled by Chinese companies.

China also produces 97% of the world’s gallium and 68% of its germanium.

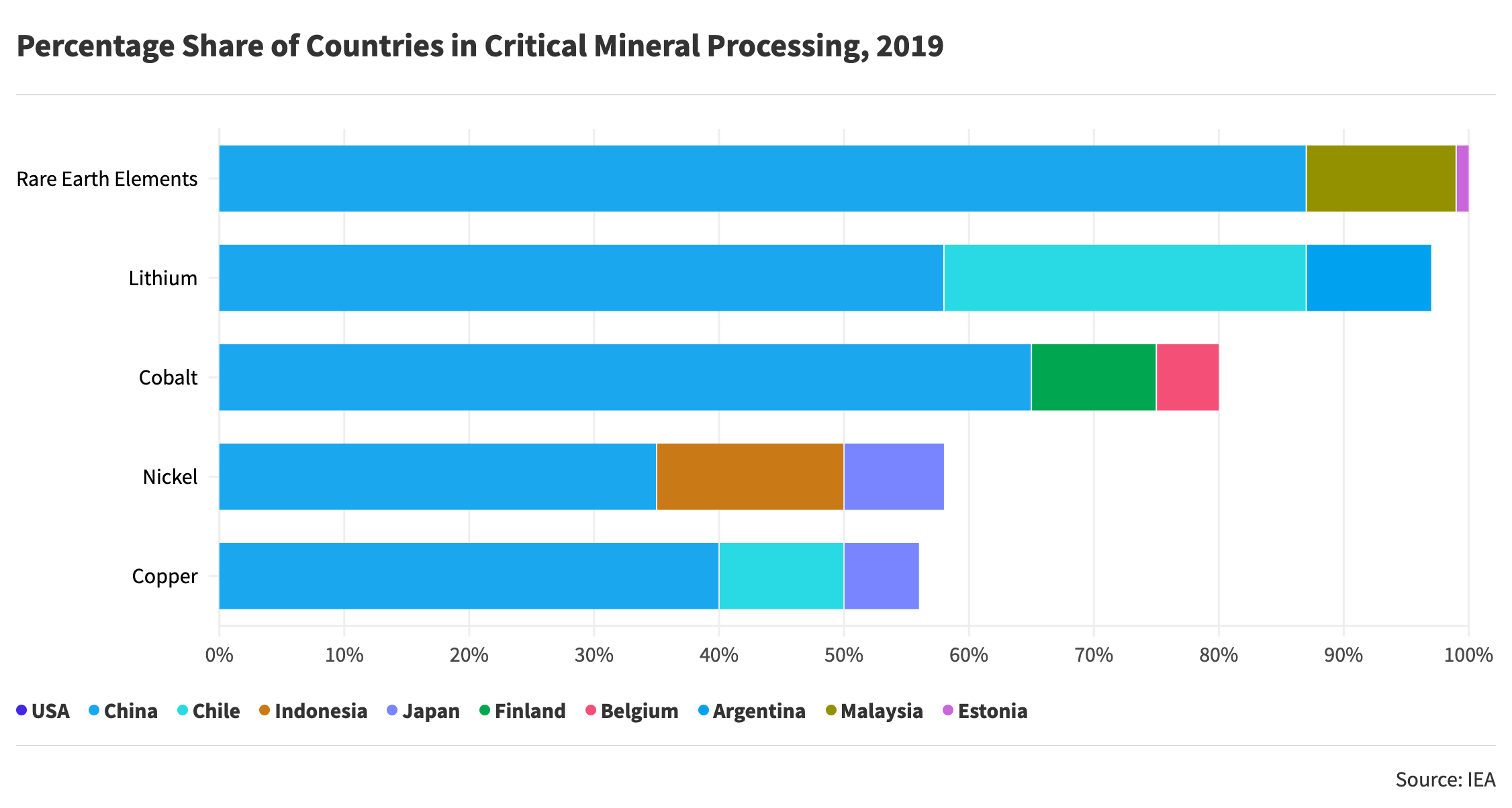

While China’s share of raw mineral production may not look overwhelming at first glance, the picture in processing is radically different.

China accounts for 90% of rare earth element processing — elements that are essential for drones, wind turbines, phones, and electric vehicles.

The West’s Problem

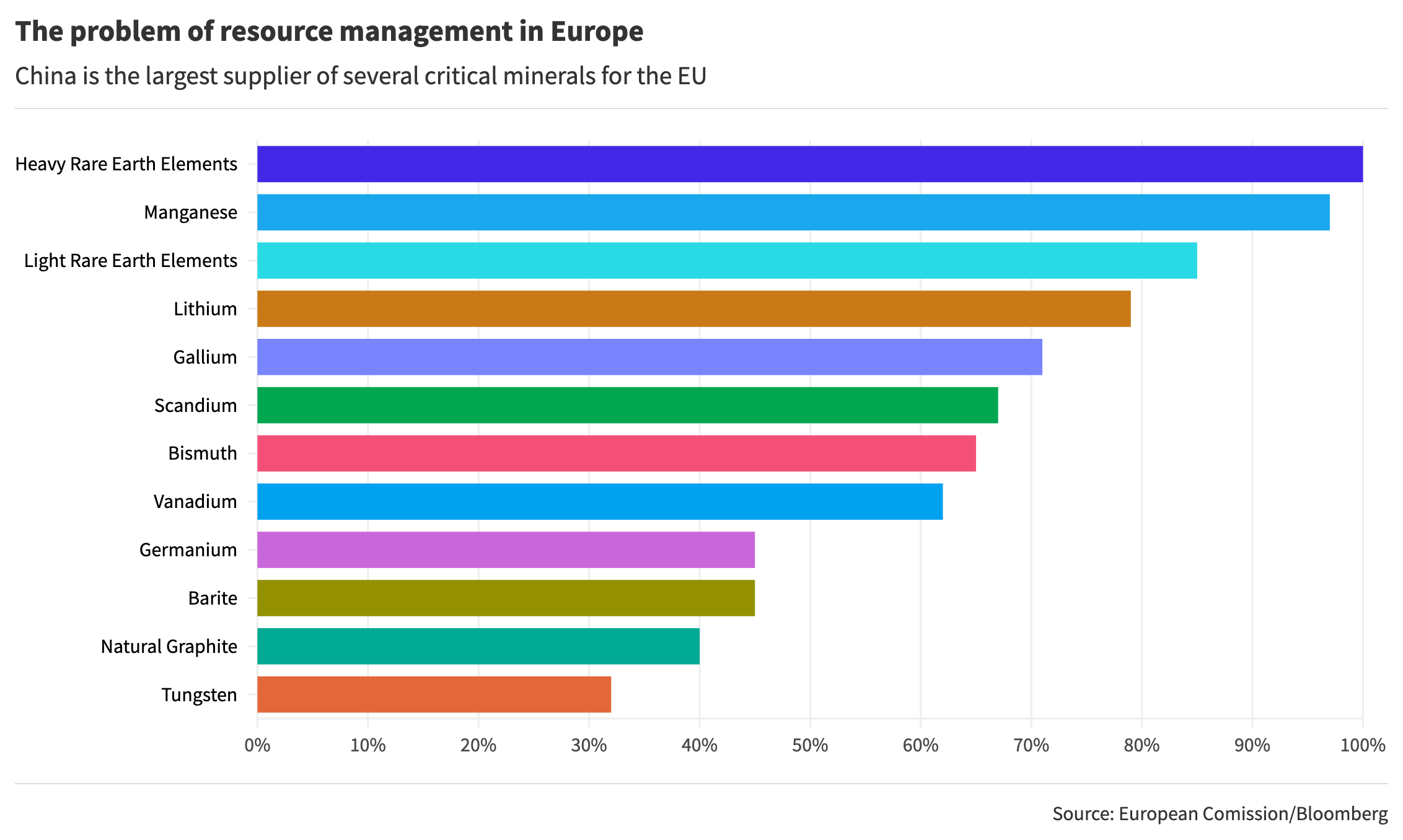

China is Europe’s primary supplier of critical minerals. Dependence on any single country always carries serious risk: during economic crises, pandemics, or social unrest, the extraction and supply of resources can be disrupted.

With China, the situation is even more complicated — it is engaged in a trade war with the US, and punitive tariffs and export restrictions are a recurring feature of the relationship.

History already offers examples of China using resources as a political weapon and disrupting supply for various reasons:

- In 2010, China banned the sale of rare earth elements to Japan, disrupting the country’s electronics sector and global magnet supply chains.

- During the COVID-19 pandemic, Chinese industrial hubs halted the supply of numerous goods, causing prices to spike sharply.

- In 2021, electricity supply restrictions in China disrupted silicon production, and within just two months prices surged by up to 300%, creating problems across multiple economic sectors.

- In July 2022, China imposed export restrictions on gallium and germanium.

China’s monopoly position allows it to effectively set prices on certain minerals, undermining the ability of competing countries to develop their own markets.

The EU has already learned a painful lesson from its dependence on Russian energy. Avoiding a repeat will require the West to take concrete action.

Counter-Moves

China and other fast-growing economies are increasingly tightening export restrictions on industrial minerals, forcing the US and European countries to scale up their own processing capacity — though securing the raw materials to process remains the harder challenge.

At the same time, Chinese companies are pushing to expand their influence further. While America is working with Canada and Australia to build cobalt supply networks, China’s reach is extending deep into African nations.

That said, Western countries do have options. The most immediate priority is encouraging mining and processing in trusted partner countries.

President Biden’s Inflation Reduction Act aims to reduce prices on raw materials needed for the energy transition and cut dependence on foreign suppliers.

The same legislation limits Beijing’s advantages in the electric vehicle supply chain — companies using components from “foreign entities of concern” will be ineligible for tax credits.

The US has also signed an investment agreement with Vietnam, which holds the world’s second-largest reserves of rare earth elements, with the explicit goal of breaking China’s monopoly.

Washington is also working on trade agreements to ensure that measures designed to boost domestic production do not shut out European and Japanese suppliers from the American market.

The EU’s Critical Raw Materials Act aims to increase funding and support for new industrial projects, as well as to build new trade alliances.

The EU is in negotiations with Estonia over building a permanent magnet manufacturing facility.

European Commission President Ursula von der Leyen also announced an investigation into Chinese electric vehicle manufacturers — thanks to state subsidies, they can produce cars cheaply, which von der Leyen argues creates an uneven playing field for European producers.

Europe and the US are also planning to establish a “buyers’ club” aimed at reaching investment agreements with producer countries. At the G7 ministers’ meeting in April 2023, participants agreed to spend $13 billion on new industrial projects.

Are these steps enough? As a starting point the moves are logical, but if Western countries want to seriously challenge China’s dominance, they will need to do far more, and faster.

China’s advantage is not geological — it is political. Any disruption to critical mineral supply, for whatever reason, would first drive up the cost of the products that rely on those resources, then ripple through the interconnected sectors of the wider economy.

Most importantly, if China maintains its monopoly position in the market, the entire global transition to renewable energy — one of the most pressing issues facing the world today, and one that arguably matters more than any political or business interest — could be put at risk.