The launch of Georgia’s first oil refinery in Kulevi was presented as a long-awaited industrial breakthrough and a step toward strengthening the country’s energy security. Yet the timing of the project, the structure of crude oil supplies, and recent trade data raise questions about the refinery’s underlying economic logic and the risks it may pose for Georgia amid tightening international oil-related sanctions.

At the center of the debate lies a broader question: what role can the Kulevi refinery play in a global oil market increasingly shaped by sanctions, compliance risks, and geopolitical tensions? This debate gained particular relevance following a recent letter from EU sanctions envoy David O’Sullivan to Georgia’s foreign minister confirming that Kulevi Port will not be included in the EU’s forthcoming 20th sanctions package after Georgian authorities and the port operator committed to strengthening compliance with EU sanctions rules.

A refinery aligned with Russian crude economics

From a commercial and technical perspective, the Kulevi refinery is highly compatible with Russian crude oil supply. Geography and economics both point in that direction: short maritime distance to Russian export ports in the Black Sea, stable availability of supply, and – since 2022 – discounted pricing of Russian oil, which appears to have been central to the project’s business model. Substituting Russian crude with alternative feedstock would present serious economic challenges. Oil supplies from Azerbaijan, Central Asia countries, or other global producers would involve longer shipping routes, higher transport costs, and potentially technical adjustments in refinery operations. Under such conditions, the refinery’s competitive advantage would be significantly reduced.

This assumption is not theoretical. It was publicly confirmed in October 2025, when Russneft, the sixth-largest oil company in Russia by crude oil production, shipped roughly 100,000 tons of Siberian Light crude from the Russian port of Novorossiysk to Kulevi, coinciding with the refinery’s launch.

Timing is equally important. The project was initiated during a period when EU sanctions did not prohibit imports of petroleum products refined in third countries from Russian crude. At that time, countries such as India, China, and Turkey were importing large volumes of discounted Russian oil, refining it domestically, and exporting petroleum products to EU markets under their own country of origin, capturing substantial margins in the process.

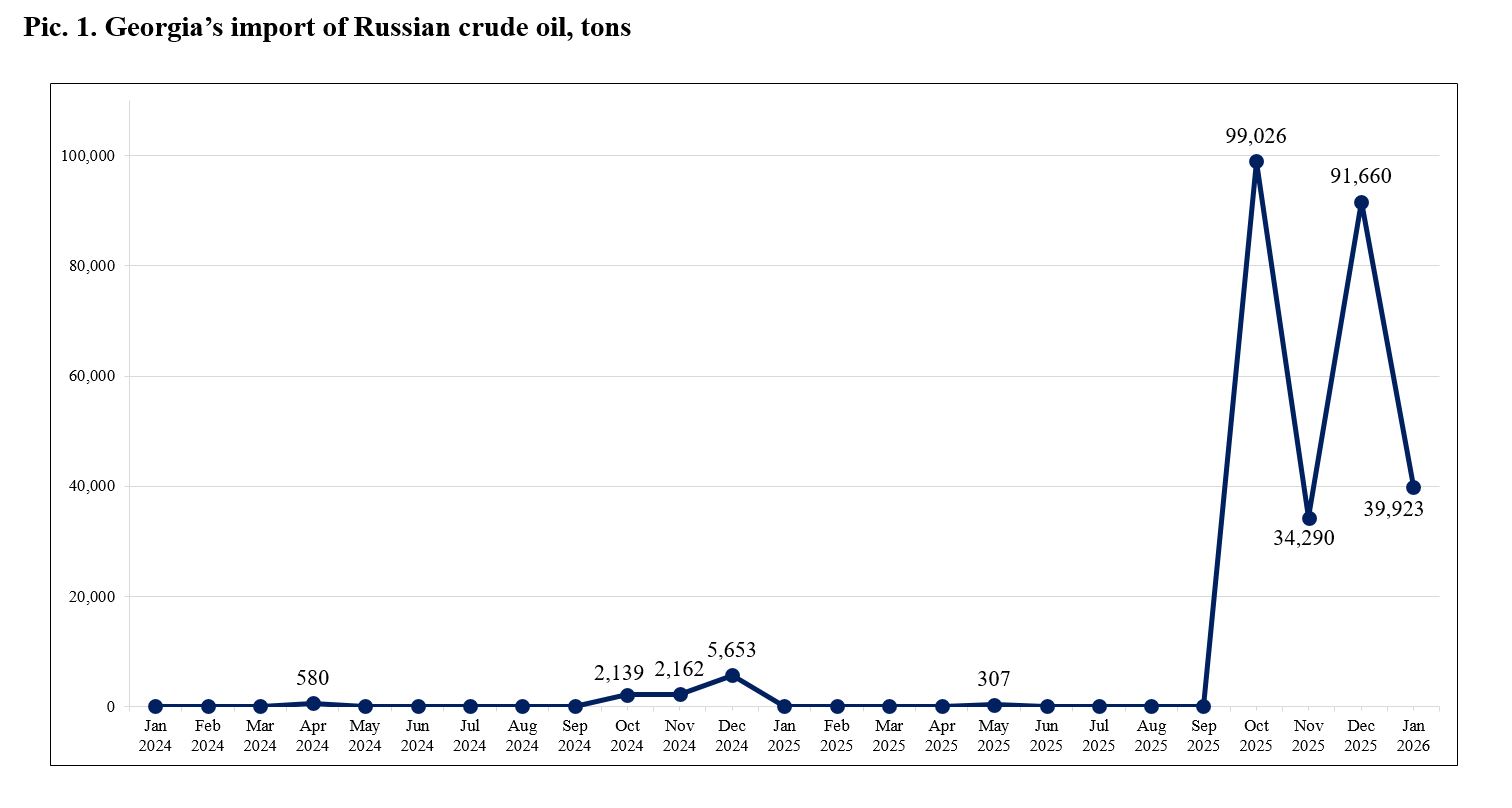

Georgia appeared positioned to replicate this model. Historically, Georgia did not import Russian crude oil in meaningful volumes. Only occasional deliveries took place, for example, around 3,000 tons in June 2023 or approximately 5,600 tons in December 2024. However, the situation changed dramatically after the launch of the Kulevi refinery. Within just four months between October 2025 and January 2026, Georgia imported approximately 265,000 tons of crude oil from Russia (Pic. 1). This represents a clear structural break in Georgia’s crude import patterns and strongly suggests that refinery operations are closely linked to Russian crude supply.

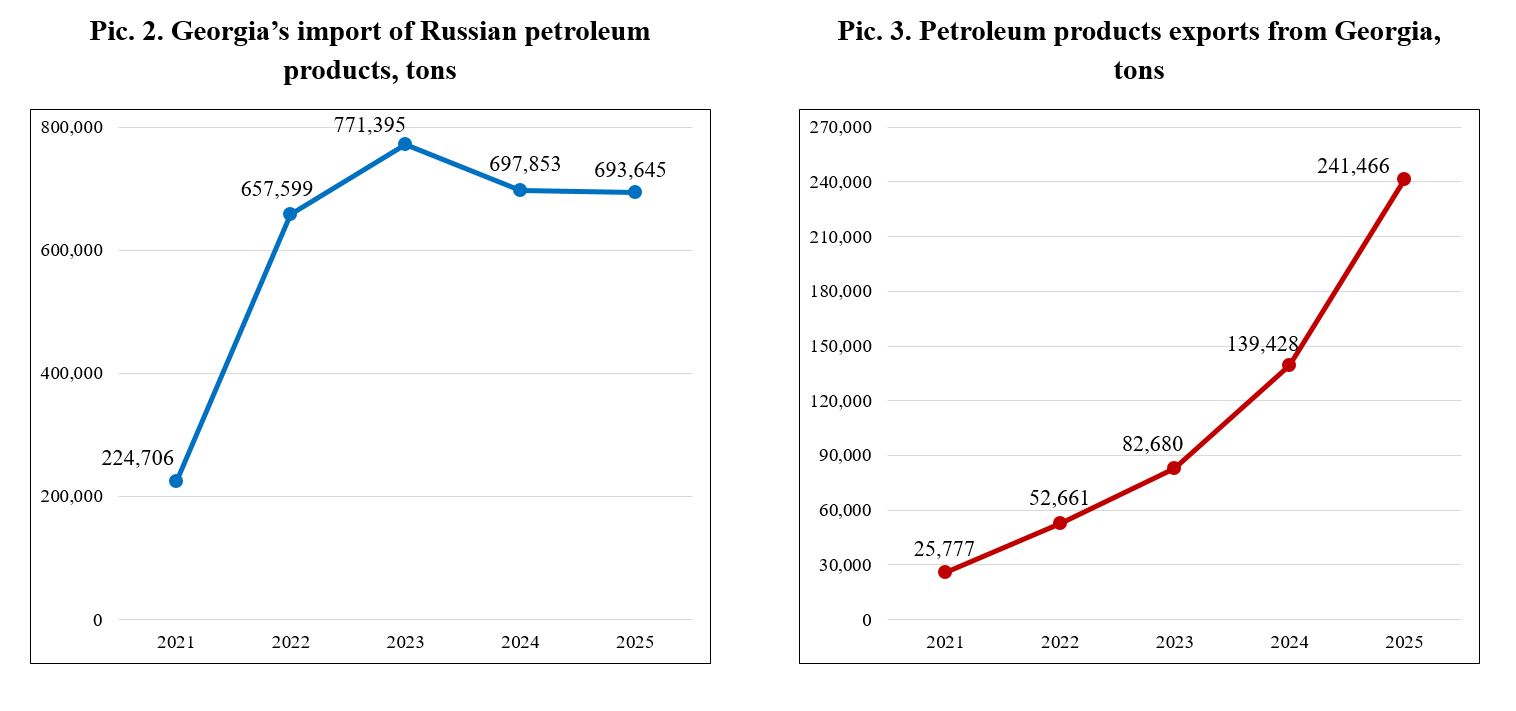

The evolution of petroleum product trade statistics reveals a broader transformation of Georgia’s role in regional oil logistics. Georgia imports significant volumes of Russian petroleum products for domestic consumption. However, these imports increased substantially after Russia’s full-scale invasion of Ukraine. Imports of Russian petroleum products rose from approximately 225,000 tons in 2021 to nearly 694,000 tons in 2025 (Pic. 2). At the same time, Georgia demonstrated a growing role as a transit and re-export hub for petroleum products. Exports volumes increased dramatically from roughly 26,000 tons in 2021 to almost 242,000 tons in 2025 (Pic. 3).

This pattern attracted attention from investigative journalists and policy analysts, as petroleum products originating from Russia were reportedly exported from Georgia under a new commercial and statistical identity.

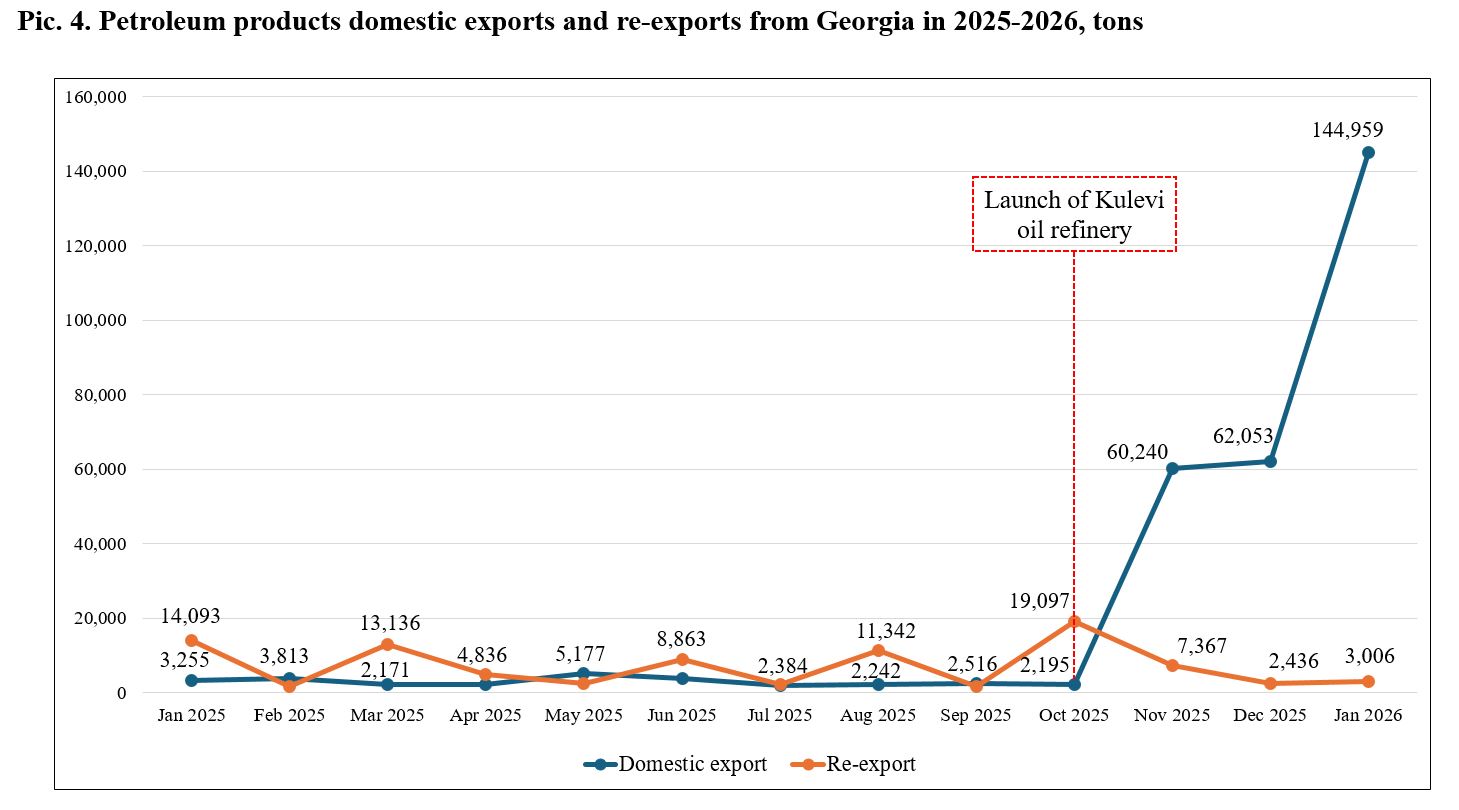

The launch of the Kulevi refinery in late 2025 appears to have altered this pattern. Instead of relying primarily on re-exports, Georgia began exporting domestically refined petroleum products. Between November 2025 and January 2026, Georgia exported approximately 270,000 tons of domestically produced petroleum products, reflecting the first large-scale refinery output recorded in the country’s modern trade statistics (Pic. 4).

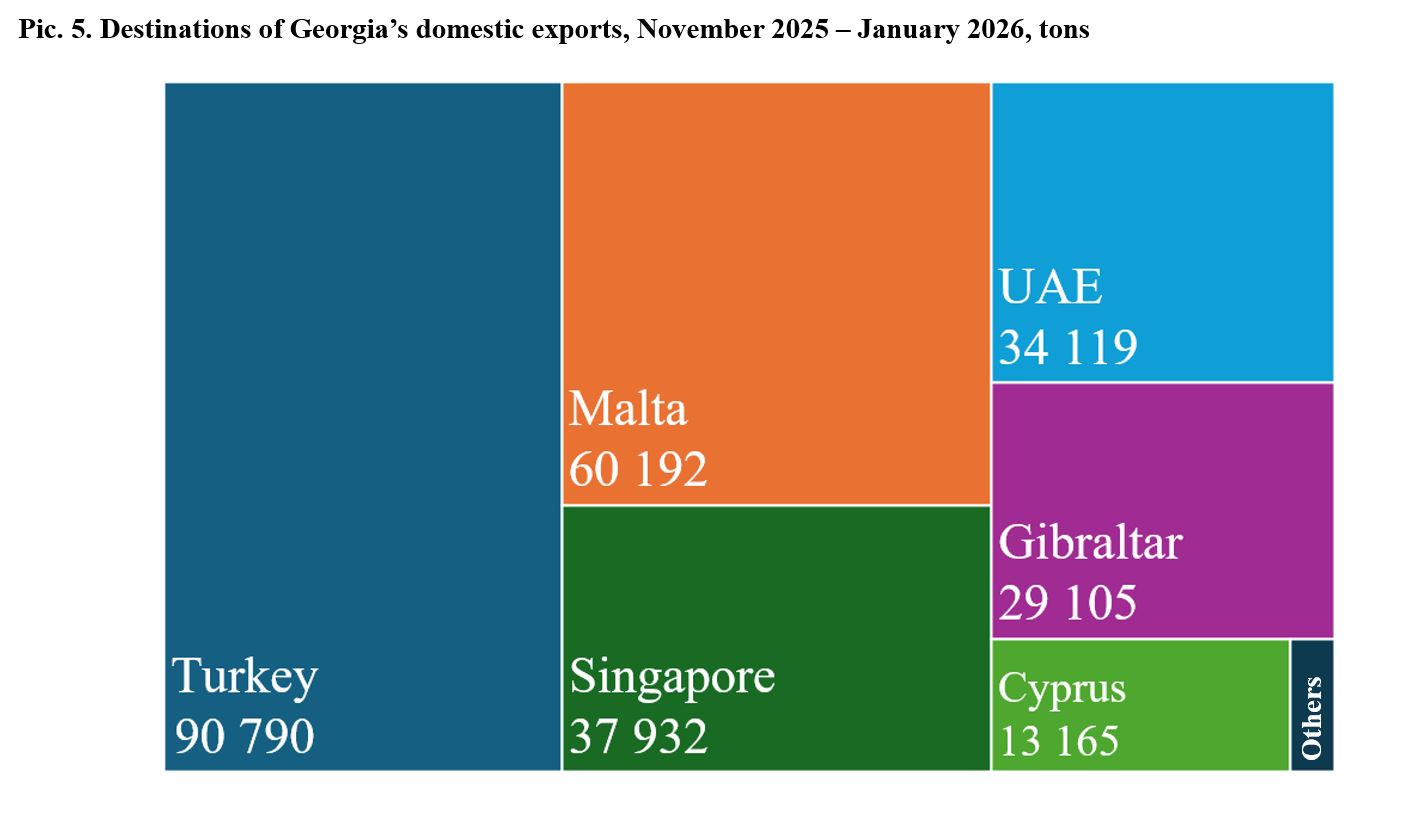

Export geography also highlights the geopolitical sensitivity of these flows. During the same three-month period, a significant share of Georgia’s petroleum product exports – approximately 103,000 tons – was directed to European markets, particularly Malta, Cyprus, and Gibraltar (Pic. 5). This export structure suggests that the refinery was initially integrated into trading routes that included European markets, despite the tightening sanctions regime (Pic. 6)

Taken together, these figures suggest a rapid transformation of Georgia’s position in the regional oil trade: from a transit and re-export platform for petroleum products toward a refining hub processing imported crude oil and exporting refined products.

At the same time, this transformation exposes Georgia to significant sanctions-related risks. Effective January 21, 2026, the European Union banned imports of petroleum products (HS code 2710, including diesel, gasoline, and fuel oil) produced from Russian crude oil in third countries. If the Kulevi refinery relies primarily on Russian crude supply, this restriction significantly limits its access to the most attractive export destination – European markets, while potentially exposing both the refinery and the port itself to secondary-sanctions risks.

The global environment that enabled such refinery-based arbitrage is now tightening. Countries such as China, India, and Turkey have already begun reducing imports of Russian crude amid rising secondary-sanctions and tariff-related risks. As a result, the external conditions that initially made refinery-based sanctions arbitrage attractive are gradually narrowing.

Shadow fleet signals and enforcement risks

The trade patterns described above also raise questions about the maritime logistics supporting these flows between Russian and Georgian ports. Tankers traveling these routes while disabling the Automatic Identification System (AIS) appear to follow patterns widely associated with so-called “shadow fleet” tactics. These practices reduce visibility, obscure routing, and complicate sanctions monitoring.

For a refinery or terminal, accepting such vessels carries significant secondary-sanctions risks. AIS manipulation and the absence of Western insurance are widely recognized red flags for enforcement authorities in the EU, the United States, and the United Kingdom. Similar patterns have already resulted in sanctions against refineries in China (e.g., Shandong and Hebei) and India (Nayara Energy).

There is also a growing trade policy risk. In the United States, a bipartisan bill under discussion proposes tariffs of up to 500% on exports from third countries that continue purchasing Russian oil. If adopted, such measures could dramatically increase the cost of participation in these trade schemes – not only for energy companies but for entire export sectors. This is particularly relevant for Georgia, which exported approximately $120 million worth of goods to the United States in 2025.

If shadow fleet voyages become systematic and recurrent, state institutions inevitably become part of a broader grey regulatory environment, including port authorities, customs services, maritime regulators, and safety agencies. Sanctions authorities are increasingly closing these grey zones across jurisdictions, limiting the long-term opportunities for sanctions circumvention.

As noted in the EU sanctions envoy’s letter, the European authorities are prepared to “impose transaction bans on enablers, such as infrastructure located in Russia and third countries, which support these activities and risk jeopardizing the effectiveness of our sanctions through circumvention”. In this context, transporting Russian crude oil outside shadow fleet networks is becoming increasingly difficult, while reliance on such networks significantly elevates sanctions-related risks.

The broader cost for Georgia

Despite its potential economic benefits, the long-term viability of the Kulevi refinery remains uncertain. The project faces constraints related to crude supply, sanctions compliance, and access to export markets. As a result, Kulevi’s operational strategy may realistically evolve along a sanctions-compliant trajectory, primarily through reorientation toward non-European markets, particularly in the Eastern Mediterranean and Asia.

Early 2026 trade data suggests that such a shift is already emerging, with shipments of refined petroleum products directed to Turkey and Singapore. However, the stability of demand in these alternative markets remains uncertain and highly dependent on broader geopolitical developments. For example, recent tensions in the Middle East have increased demand in Asian markets for energy supplies from alternative sources, potentially supporting short-term export opportunities for refineries such as Kulevi. Yet reliance on such volatile and externally driven factors cannot provide a stable or sustainable foundation for long-term industrial strategy.

More fundamentally, the economic logic of the project raises concerns. The construction of a domestic oil refinery can, in principle, generate significant benefits for Georgia, including job creation, investment inflows, technology transfer, and the development of industrial capabilities. However, a business model heavily dependent on a single external supplier, particularly one that is politically unpredictable, engaged in military conflict, and subject to extensive international sanctions regimes, introduces a high level of strategic vulnerability.

Beyond these economic and operational constraints, the most serious exposure for Georgia lies in political and reputational risks. If Kulevi becomes perceived internationally as a hub facilitating sanctions circumvention, Georgia risks association with high-risk segments of the global oil trade. Countries that repeatedly appear in investigative reporting, NGO monitoring, or regulatory risk assessments inevitably attract increased scrutiny from the EU, the UK, the United States and international financial institutions. This scrutiny often translates into stricter compliance requirements for ports, banks, insurers, trading firms, and logistics companies, raising transaction costs across the economy.

With the launch of the Kulevi refinery, Georgia faces the same strategic dilemmas as other third countries refining Russian crude for onward export. The difference lies primarily in scale and resilience rather than principle. Larger economies can absorb reputational damage and regulatory pressure more easily. For Georgia, however, similar exposure carries disproportionately higher political and economic risks, given its reliance on Western markets, finance, and institutional trust.

Georgia has invested heavily in its image as a reliable logistics hub aligned with Western regulatory and compliance standards. Persistent links to shadow fleet activity and sanctions circumvention patterns risk undermining this positioning and creating additional friction in relations with Western partners, including on the path toward EU integration.

In this context, the long-term costs of reputational damage and regulatory isolation may ultimately outweigh the short-term commercial gains that projects such as the Kulevi refinery initially promised. The central question for Georgia is therefore not only whether Kulevi can operate profitably, but whether its underlying business model remains compatible with the country’s broader economic and geopolitical priorities.

PhD, Professor of Management, Caucasus University

PhD, Professor of Accounting and Finance, Caucasus University